The Policy

Margin lending is a controversial method of investment where an investor borrows funds to acquire shares, which are then used as security for the loan. The financier (typically a bank) may ‘call in’ the loan and sell the secured shares where the investor’s loan to value ratio reaches a prescribed limit, due to a drop in share price.

The Position

Margin loans are offered by most financial institutions and considered common practice in the market. According to RBA estimates, margin lending dramatically increased in Australia from 2000, with the total value of margin loan accounts peaking at $41.16 billion in December 2007, before the GFC took its toll on the economy.

Margin lending has steadily decreased since the GFC an as at December 2017, there are approximately 126,000 margin loan accounts in Australia with a collective value of $11.45 billion.

The Argument

Despite the reduction in margin lending, financiers still tout the practice as an effective means of scaling up investments and accelerating returns. Given the scope of margin lending, proponents also argue it is a vital tool for unlocking new investments and stimulating the economy.

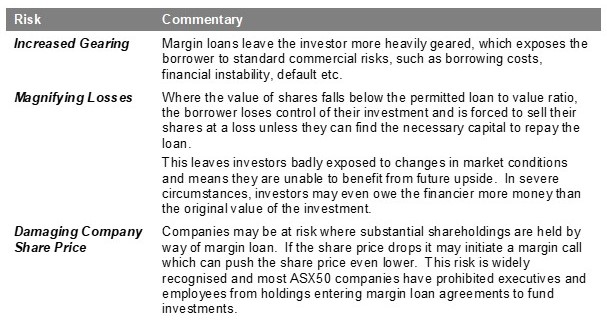

However, margin loans have been widely criticised due to several key risks:

The steady decrease in collective margin lending is evidence of the hangover left by the GFC and the reluctance of investors to expose themselves to heavily geared, and risky investments. Despite this, margin lending will likely remain an investment tool of choice for some investors in the current low interest landscape.

Further Information

- RBA statistics on margin lending

- ASIC Money Smart fact sheet on margin lending